In 2024, Europe’s market for renewable power purchase agreements (PPAs) is poised for substantial growth. Moreover, major mergers and acquisitions (M&A) also happened in the region, targeting energy companies. These key developments indicate renewed investor interest in renewable energy after a slow first quarter.

The Surge of High-Value European Green Energy Deals

The year 2023 was the busiest and most dynamic period in Europe’s renewable energy power purchase agreement history. Yet, the market is now entering what experts dubbed its ‘Golden Era’.

Corporate buyers secured 21 TWh/year of green electricity from 10 GW of new projects in the first five months of 2024, maintaining a pace similar to 2023, according to S&P Global Commodity Insights.

The number of deals increased to 145, compared to 94 in the same period of 2023, indicating more players entering the market. The growth was primarily driven by 10.2 TWh/year of wind PPAs in northern Europe and 7.5 TWh/year of solar PPAs, mainly in Spain.

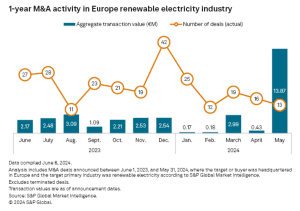

For the same period, there were three major European M&As targeting energy companies. The largest deal involved US-based Energy Capital Partners acquiring British renewable energy firm Atlantica Sustainable Infrastructure, with a transaction value of €7.25 billion.

Energy Capital will purchase all Atlantica shares with Atlantica’s largest shareholder, Algonquin Power & Utilities, supporting the deal. The transaction is expected to close by early 2025, after which Atlantica will become privately held, delisting from public markets.

The second-largest deal saw Canadian investor Brookfield Asset Management and co-investor Temasek proposing to acquire a majority stake in Neoen SA, an independent renewable energy producer. Neoen has about 8 GW in operation and under construction, plus 20 GW in development.

After Brookfield’s Neoen bid announcement, JP Morgan analysts noted that investors appeared to be willing again to invest their money in green energy development pipelines.

These high-value deals highlight a robust interest in renewable energy, underscoring the sector’s importance not just in Europe but in global energy strategies and investor portfolios.

Market Dynamics, Price Trends, and Regional Challenges

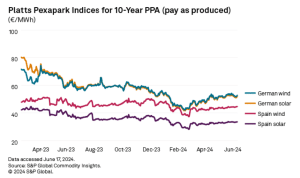

However, deal prices have declined due to lower electricity spot and forward prices, as S&P Global reported.

Iberian capture prices reached record lows this spring, influenced by bearish fundamentals and increasing solar capacity. In Germany, May’s solar capture price dropped to its lowest since summer 2020, although forward contracts recovered, with the benchmark German year-ahead power contract rising almost 50% from its February lows.

Spain and Italy face unique challenges. In Spain, despite strong corporate interest, volatile market conditions and high interest rates hindered PPA contracting.

Insufficient grid capacity also posed challenges, a problem shared with Italy and Germany. In Italy, central permitting delays have slowed down project authorization, and restrictive auction systems further complicate the market.

Germany is expected to compete closely with Spain for PPA leadership in Europe. In the first five months of 2024, Germany signed 21 deals for 2 GW of capacity, focusing on utility-scale solar and offshore wind projects.

Despite regulatory uncertainties, Germany’s large industrial base and tech sector drive PPA demand. New corporate sustainable reporting rules and mandatory datacenter requirements are additional demand drivers.

In the UK, the government-run contract for difference (CFD) auctions are highly attractive, potentially crowding out private sector deals. However, the ongoing Review of Electricity Market Arrangements (REMA) adds uncertainty, causing some market participants to pause activities.

Sectoral Shifts and New Opportunities

While Brookfield has the financial capacity for large-scale deals, few investors can match such substantial investments. Initially, oil majors were expected to be significant players in the renewable energy sector.

However, the focus on energy security since Russia’s invasion of Ukraine has shifted their priorities. Recently, Norwegian state-owned power producer Statkraft AS completed a €1.8 billion acquisition of Spanish group Enerfín SA.

Additionally, several privately owned developers are anticipated to enter the market this year.

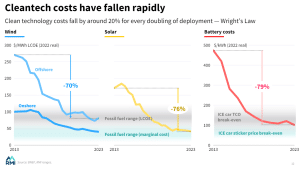

Market analysts project that this trend will continue as the cost for deploying renewables are falling significantly. As seen below, RMI data shows that costs drop by around 20% for every doubling of deployment.

Though tech companies remain the leading buyers of PPAs, but the consumer goods, industrial, chemicals, and utility sectors are also emerging as significant offtakers. The rise of artificial intelligence computing power creates new opportunities, with countries like the Nordics and Iberia seeing increased activity.

Spain, in particular, is becoming a key hub for data centers due to favorable conditions like low prices, low taxes, and renewables access.

The reform of the EU’s electricity market aims to broaden access to PPAs, with government support crucial to make these PPAs financeable.

Overall, 2024 is shaping up to be a pivotal year for Europe’s green power deals, driven by increased corporate commitment to renewable energy, the same trend happening in the U.S., despite facing significant regional and market-specific challenges.

- SEO Powered Content & PR Distribution. Get Amplified Today.

- PlatoData.Network Vertical Generative Ai. Empower Yourself. Access Here.

- PlatoAiStream. Web3 Intelligence. Knowledge Amplified. Access Here.

- PlatoESG. Carbon, CleanTech, Energy, Environment, Solar, Waste Management. Access Here.

- PlatoHealth. Biotech and Clinical Trials Intelligence. Access Here.

- Source: https://carboncredits.com/2024-is-the-golden-era-for-europes-renewable-energy-heres-why/